Driving operational convergence and high-performance execution

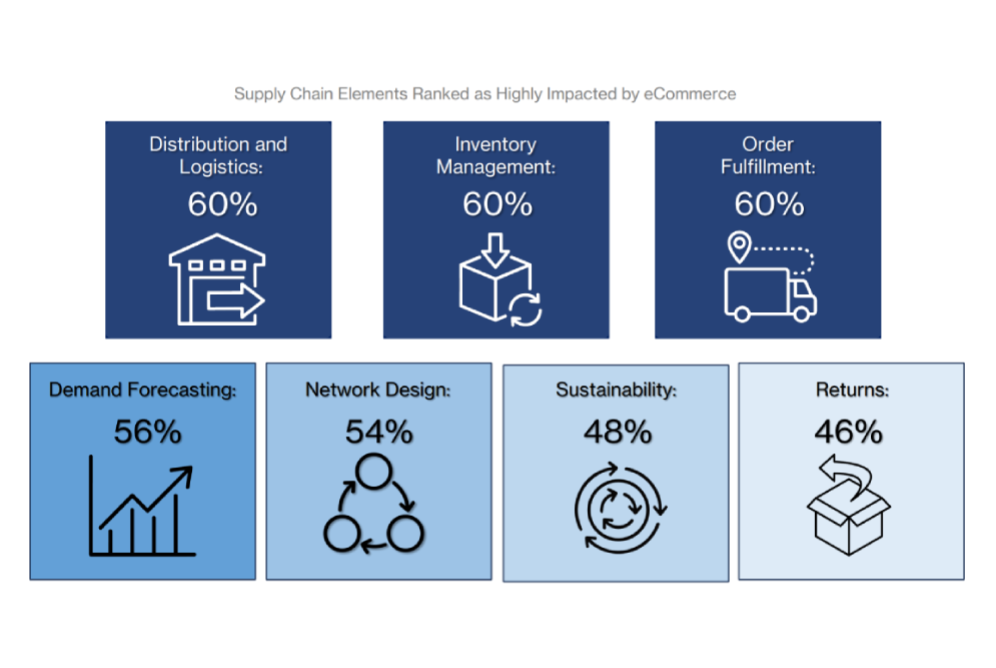

When observing the impact of the eCommerce growth within the supply chain, this year’s results show clear convergence around execution.

Distribution and logistics, inventory management, and order fulfillment all stand at 60%, with demand forecasting (56%) and network design (54%) close behind.

Unlike last year, where distribution and fulfillment were also top of mind but with a wider spread, the tighter clustering in 2025 suggests that companies are shifting their focus to high-performance execution.

Based on the 2025 survey respondents, the impact of eCommerce is no longer concentrated in isolated points of pressure, but it’s now embedded across the supply chain's operations.

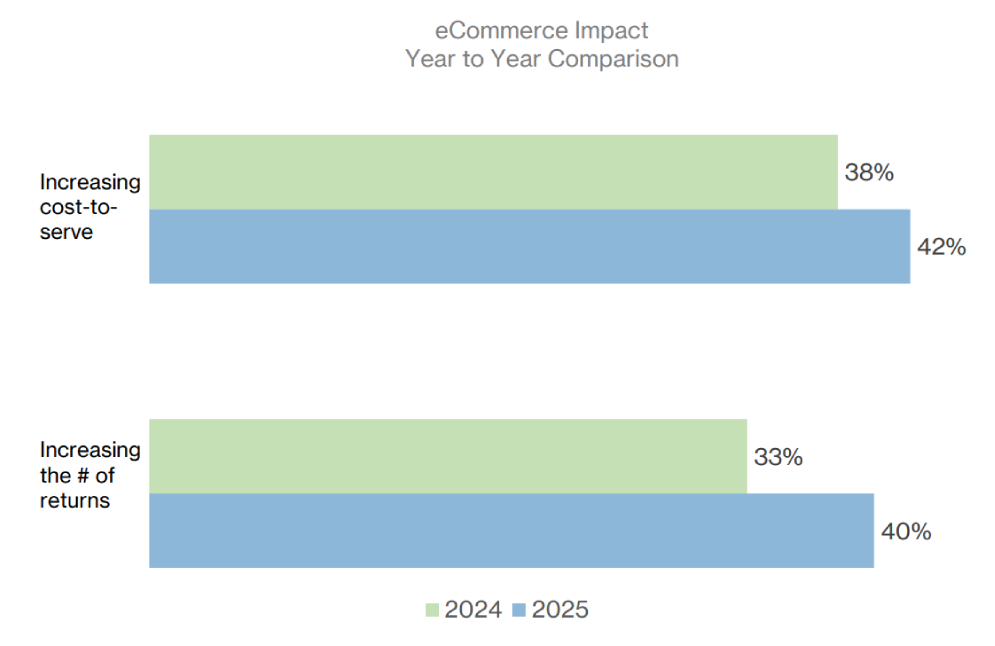

Sustainability and returns management are also rising in importance (48% vs 27% and 46% vs. 38% respectively), reflecting growing attention to the complexity that eCommerce and seamless returns bring to supply chains.

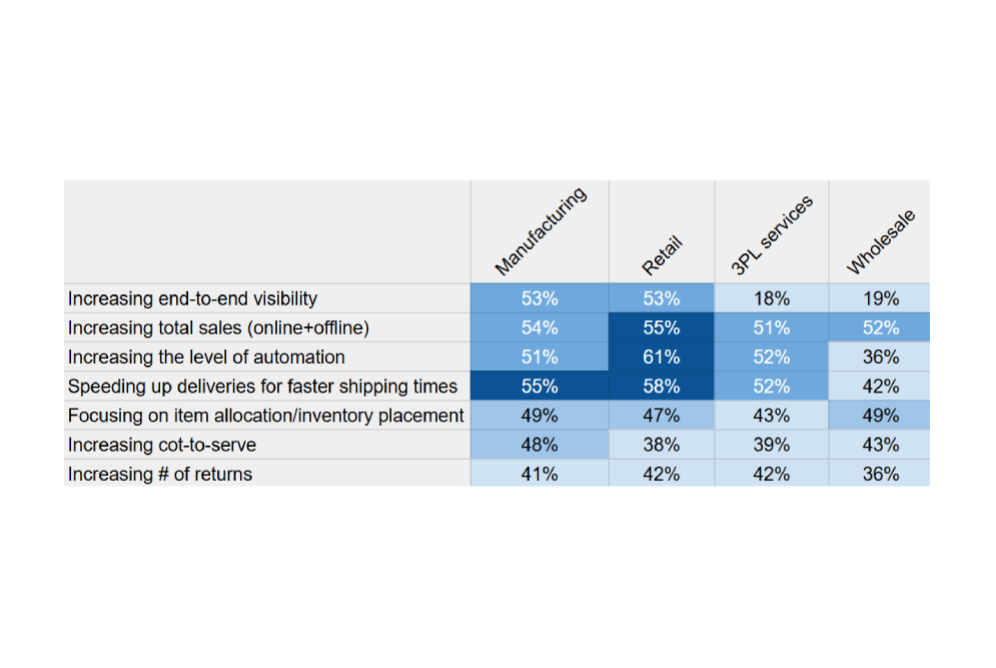

That said, once we break it down by type of business, we observe both shared pressures and meaningful differences in how each segment experiences growth. End-to-end visibility is the clear differentiator.

While manufacturing and retail both report a strong eCommerce impact (53% of respondents), third-party logistics providers and wholesalers report a minor impact. On the other hand, total sales growth is the most evenly felt impact across all four segments. Retail leads on automation at 61%, reflecting the sector’s ongoing investment in improved efficiency and performance.

When compared with other eCommerce impacts, cost-to-serve and returns sit in the lower range across all types of businesses.

This table compares operational priorities across four industries: Manufacturing, Retail, Third-party logistics services, and Wholesale. Each row lists a business objective along with the percentage of respondents in each industry who identified it as a focus area.

Across all four industries, increasing total sales (both online and offline) and speeding up deliveries are among the highest priorities, with results generally in the low-to-high 50 percent range. Retail reports the highest focus on automation at 61 percent. Manufacturing and Retail both report strong emphasis on end-to-end visibility at 53 percent, while Third-party logistics and Wholesale report lower emphasis in this area, at 18 and 19 percent respectively.

Inventory allocation and placement show fairly similar levels of importance across industries, ranging from 43 to 49 percent. Increasing cost-to-serve is cited by roughly 38 to 48 percent depending on industry, with Manufacturing reporting the highest level. Increasing the number of returns is the lowest-ranked priority overall, with percentages ranging from 36 to 42 percent across industries.

Overall, the data shows strong alignment across sectors in prioritizing sales growth, delivery speed, and automation, with more variation in visibility and cost-related focus areas.