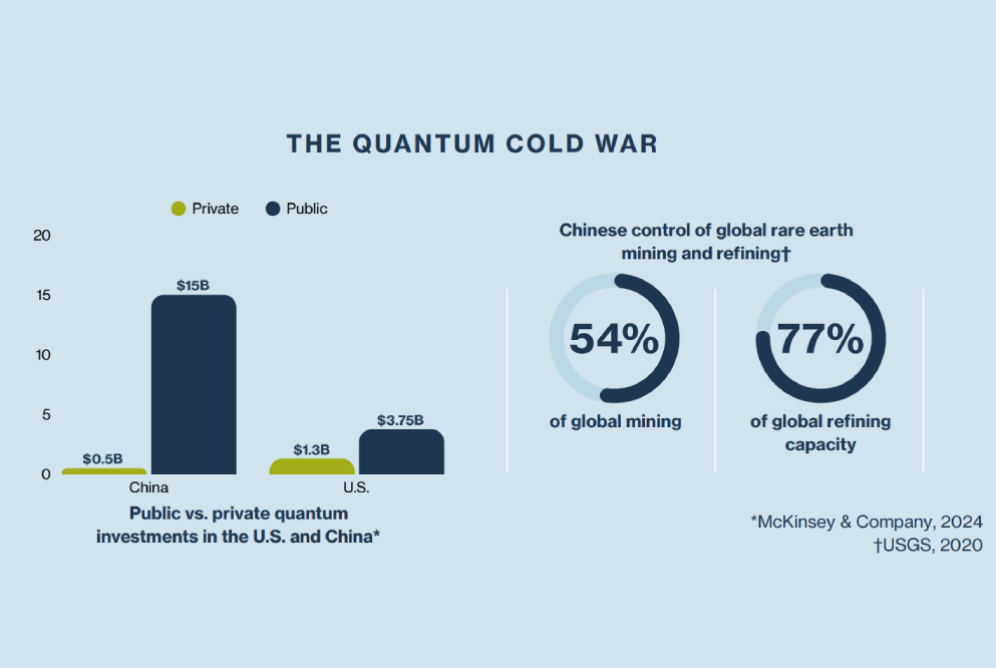

Quantum computing has become a strategic priority for economic competitiveness and national security, with the United States and China investing heavily in what many describe as a “quantum cold war.” While the U.S. leads in private investment and international patents, China’s dominance in rare earth mining (54%) and refining (77%) highlights growing supply chain dependencies that could constrain future hardware development.

This research maps 160 companies and critical materials across four supply chain tiers, using graph theory, agent-based modeling, predictive analytics, and robustness simulations to evaluate systemic risk. The findings show that while the ecosystem can absorb random disruptions, the loss of a small number of highly connected firms significantly weakens overall stability. The report outlines practical steps to strengthen resilience—from trusted trade partnerships to multi-source strategies and continuous monitoring of emerging technologies.

Download the full report to understand the risks and build a more resilient quantum supply chain.

The Challenge

Quantum computing has emerged as a strategic frontier for U.S. economic competitiveness and national security.

A "quantum cold war" is escalating between the U.S. and China, with China committing massive public investment while the U.S. leads in private funding. The U.S. currently leads in international patent filings, though China is rapidly closing the gap, driven by aggressive domestic filings and national policy support. The U.S. maintains a qualitative edge and international reach while China accelerates in volume and state-backed infrastructure.

As demand for quantum machines grows, essential materials such as rare earth elements and helium isotopes become key bottlenecks. Other challenges in scalability, error correction, and component fabrication create an urgent need to map the structure, resilience, and strategic vulnerabilities of the global supply chain for quantum computing hardware.

This image presents a comparative view of quantum computing investment and upstream material concentration. A bar chart contrasts China and the United States across private and public funding. China shows $0.5 billion in private investment and $15 billion in public investment, while the United States shows $1.3 billion in private investment and $3.75 billion in public investment (source: McKinsey & Company, 2024).

Alongside the investment chart, a second set of graphics highlights China’s role in rare earth supply chains. The visuals indicate that China accounts for 54% of global rare earth mining and 77% of global refining capacity (source: USGS, 2020), underscoring its significant position in critical material processing.

The Research

To evaluate the stability of quantum computing supply chains, we mapped a list of 160 companies and critical materials across four supply chain tiers:

Tier 1: firms directly building quantum processors

Tier 2: firms providing support infrastructure and enabling systems

Tier 3: subsystem integrators and component-level suppliers

Tier 4: upstream suppliers of raw materials

This allowed us to structure our model of the quantum ecosystem along a sequential flow of production, with each company or entity representing a node in the network.

We then employed a multi-disciplinary approach to evaluate risk:

- Graph theory: applied to identify "hub" nodes and calculate degree centrality to find the most structurally important firms

- Agent-based modeling: used to simulate how upstream shocks (such as a disruption at a major chipmaker) ripple through the network based on firm behavior and inventory buffers

- Predictive analytics: augmented firm data with 6-digit HS code trade mappings to link technical capabilities to global macroeconomic flows

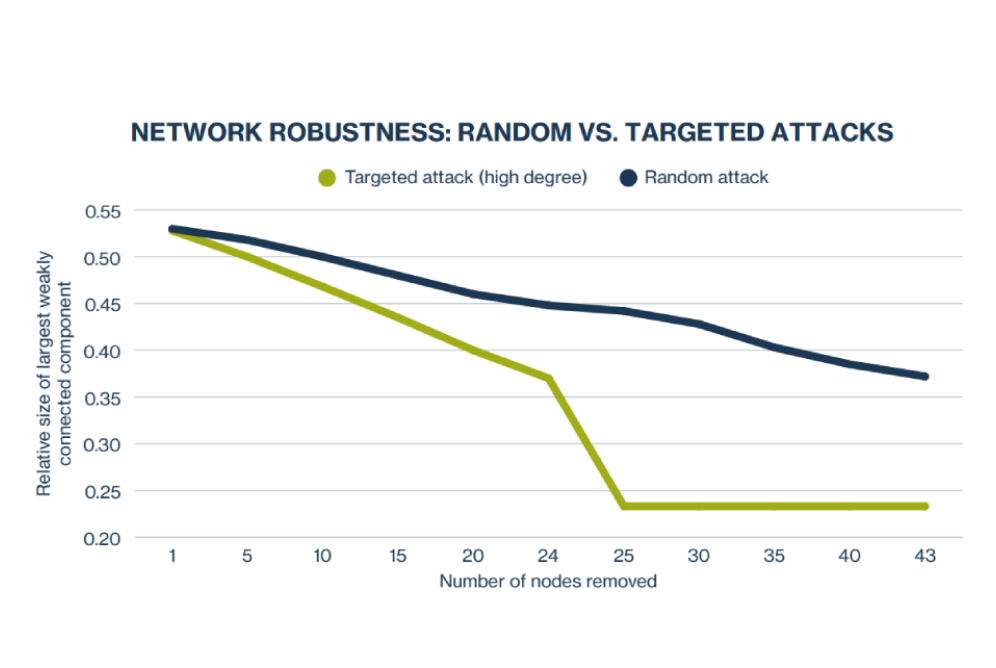

- Robustness simulations: tested the network against "random attacks" versus "targeted attacks" on high-centrality hubs

This chart illustrates the resilience of the quantum supply chain network under different disruption scenarios. The x-axis shows the number of nodes removed from the network, while the y-axis represents the relative size of the largest weakly connected component. Two lines are plotted: a blue line for random node removal and a green line for targeted removal of high-degree (highly connected) nodes.

Both lines begin at one node removed, with the network at approximately 0.5 relative size. As additional nodes are removed, the blue line declines gradually, ending around 0.37, indicating steady but manageable degradation under random disruptions. The green line follows a similar early trajectory but experiences a sharp drop at approximately 24 nodes removed, falling to about 0.37 before leveling off near 0.24 at 25 nodes removed. The accompanying caption explains that the simulations show gradual degradation under random disruptions, but a rapid collapse when highly connected hubs are removed, highlighting structural fragility within key supplier tiers.

Network robustness simulations indicated that the system degrades gradually under random attacks (blue line) but collapses rapidly when high-centrality nodes are targeted (green line), revealing structural fragility in key supplier tiers.

Recommendations

Our analysis confirms that the quantum ecosystem is highly susceptible to targeted disruption. While the network shows resilience against random failures, the removal of just ~25 top-connected nodes causes a sudden systemic collapse. High-centrality firms act as critical intermediaries; a compromise of these hubs could fragment the entire industry.

To address these risks and build a resilient quantum future, we offer the following recommendations:

- Map, monitor, and simulate quantum supply chains: Establish a dedicated initiative to map firm-level quantum supply chains using open standards. Expand the available dataset and simulation tools to proactively stress-test the system and identify critical chokepoints.

- Secure trusted trade alliances: Build resilient sourcing through bilateral quantum manufacturing partnerships with trusted nations (e.g., Japan, Finland, Canada) in domains such as high-vacuum optics and superconducting components.

- Redundancy and interoperability: Pursue multi-source procurement strategies and monitor material dependencies to reduce single-point failure risk

- Continuously scan emerging architectures: Build text mining and AI tools to monitor publications and patents from top quantum scientists and leading startups that will allow identification of strategic dependencies and enable planning for future scenarios for quantum computing supply chains.